I feel I have lived through an era of great changes. The pace of change can seem accelerated if you travel or emigrate because various geographical regions act as different slices in time. I have had the benefit (or the misfortune) of multiple emigrations. With that, coupled with my advancing years, I feel as though I have seen a lot. Most of what I have seen fills me with a foreboding of gloom and doom. Perhaps it is merely the pessimism characteristic of an unduly cynical mind, or perhaps it is the true decay of our global ethical standards.

On the positive side, the pace of change is indeed fast and furious. This is the kind of change you like — you know, vinyl to spool tape to cassette to MP3 to iPod kind. Or the land-line to satellite to cell to Skype to Twitter kind. However, along with this positive and obvious track of changes, there is an insidiously slow and troubling track creeping up on us. It is n this context that I want to reuse the over-used allegory of the frog-in-a-pot.

If you put a frog in hot water, it will jump out of the pot and save its skin. But if you place the frog in cold water, and slowly heat up the pot, it won’t feel the change and boil to death. The slowness of change is deadly. So let me be the frog with delusions of grandeur; allow me to highlight the unhealthy changes accumulating around us. You see, along with the technological miracle that we are living through, there is an economic or financial nightmare that is spreading its tentacles over all aspects of our social and political existence, transfixing everything in place in its vice-like grip. Slowly. Very slowly. Because of this invisible hold on us, with every iPod we buy, we (the middle-class) take a couple of dollars from the very poor and give it to the very rich. We don’t see it that way because some of us make a few cents in the process. The Apple store franchisee makes a few cents, the employee-of-the-month gets a token raise, an apple developer may enjoy a nice vacation, or a senior executive might get a new jet, the economy of the country goes up a notch, NASDAQ (and so everybody’s pension) goes up a tiny fraction — all are happy, right?

Well, there is this little question of the packaging material that may have killed part of a tree somewhere, in Brazil, perhaps, where people don’t know that the trees belong to them. May be a little bit of pollution escaped into the air or a river in China where the locals haven’t realized that these resources are their heirlooms. May be some moderately toxic junk ended up in a landfill in Africa somewhere where they haven’t quite grasped the concept of land ownership. It may have cost a developer in Bangalore or a call-center girl in Manilla an hour or two more than it should because they don’t know that their time is a resource bought low and sold high in markets they don’t see or know of. It is from these distant places and phantom people that we pick up a couple of dollars and pass on to the equally distant corporate coffers and stock markets. We take what is not ours from the unknown owners to feed the avarice of unseen players. And, like Milo Minderbinder would say, everybody has a share. This is the modern capitalism of the corporate era, where we have all become tiny cogs in a giant wheel inexorably rolling on to nowhere in particular, but obliterating much in the process.

The problem with capitalism as an economic ideology is that it is pretty much unopposed now. Only through a conflict of ideology can a balance of some sort emerge. Every conflict, by definition, requires adversaries, at least two of them. And so does an ideological struggle. The struggle is between capitalism and communism (or socialism, I’m not sure of the difference). The former says we should lay off the markets and let greed and selfishness run its course. Well, if you don’t like the sound of “greed and selfishness,” try “ambition and drive.” Associate it with words like freedom and democracy, and this “Laissez-Faire” ideology a la Adam Smith is a winning formula.

Standing in the other corner is the opposing ideology, which says we should control the flow of money and resources, and spread happiness. Unfortunately this ideology got associated with nasty words like totalitarianism, bureaucracy, mass murder, killing fields of Cambodia etc. Little wonder that it lost, save for this economic powerhouse called China. But the victory of China is no consolation for the socialist camp because China did it by redefining socialism or communism to essentially mean capitalism. So the victory of capitalism is, to all intents and purposes, a slam dunk. To the victors belong to spoils of history. And so, the socio-politico-economic ideology of capitalism enjoys the mellifluous association of nice words like liberty, equal opportunity, democracy etc., while communism is a failed experiment relegated to the “also-ran” category of ideologies such as fascism, Nazism and other evil stuff. So the battle between capitalism and the occupy-wall-street movements is pathetically asymmetric.

A battle between two well-matched opponents is nice to watch; say, a match between Djokovic and Federer. On the other hand, a “match” between Federer and me would be exciting only to me — if that. If you are into violent entertainment, a boxing match between two heavy weights would be something interesting to watch. but a brawny boxer beating the living daylights out of a two-year-old would only fill you with revolt and disgust (which is similar to the feeling I had during the ’91 Gulf War).

Don’t worry, I’m not about to defend or try to revive socialism on this blog, because I don’t think a centrally controlled economy works either. What worries me is the fact that capitalism does not have a worthy adversary now. Shouldn’t it worry you as well? Corporate capitalism is beating the living daylights out of everything that one might call decent and human. Should we ignore and learn to love our disgust just because we got a share?

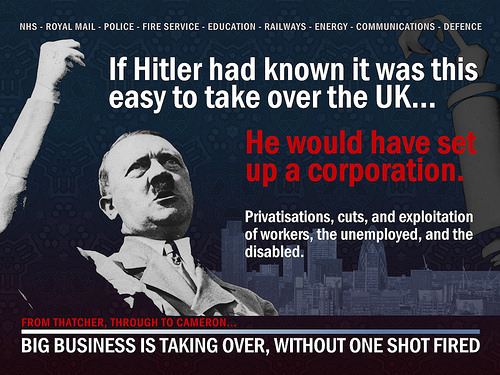

Photo by Byzantine_K